Appeal against High Court ruling on disproportionate criminal records disclosure scheme scheduled

Since the High Court ruling in January, which found that the current criminal record disclosure scheme for standard/enhanced checks was disproportionate, lots of people have been asking us what would happen next.

We’re now in a position to say that the Government has appealed against the High Court ruling (which to some extent we expected) – this means that the case will go up to the Court of Appeal. The case is being heard with three other cases that involve the ‘type of offence’ exclusion (which is another area we think needs to change).

The case has been listed to be heard in February 2017 with a judgement expected later in the year.

In the meantime, nothing changes. The current DBS filtering system remains in force. If the outcome of the appeal goes the right way from our perspective, the government would need to look at extending the filtering process.

Although the review has only just been published, the date on the review is November 2015, which seems to reflect when the review was completed. After that point, the DBS appear to have set about responding to the recommendations.

Of particular interest to us was that it was good to see the review recommend that the DBS consider situations where oral representations (instead of just written ones) could be made by those at risk of being barred. This is something that we featured as an update to our information site back in February of this year.

The review also recognised how the letters and factsheets sent out by the DBS are not as effective as they might be in:

encouraging those at risk of barring to participate in the process and to make representations, or

communicating the outcome in a fashion that is both easy to understand and accurate.

The review recommended a ‘mini-review’ and suggested working closely with those who have experience of would be barrees, such as Unlock. The DBS has since done some of this work and we’ve engaged with them to improve the information and communications with those subject to the barring process.

In January 2016, the Prime Minister asked David Lammy MP to investigate evidence of possible bias against black defendants and other ethnic minorities.

Insurers are not following good practice when dealing with criminal records

Last month, the Financial Conduct Authority published an occasional paper on access to financial services. I fed into this work, particularly focusing on the issues people with convictions face in accessing insurance. So it was good to see the authors include an especially challenging section of the report focused at a lack of buy-in to industry guidance.

There was heavy reference to the work that Unlock has done with the Association of British Insurers (ABI), including developing good practice, but highlighted how:

“it is still commonplace for proposal forms to have questions such as “have you ever been convicted””

The ABI guidance states that it is good practice to refer only to ‘unspent’ convictions, so clearly insurers are not doing this.

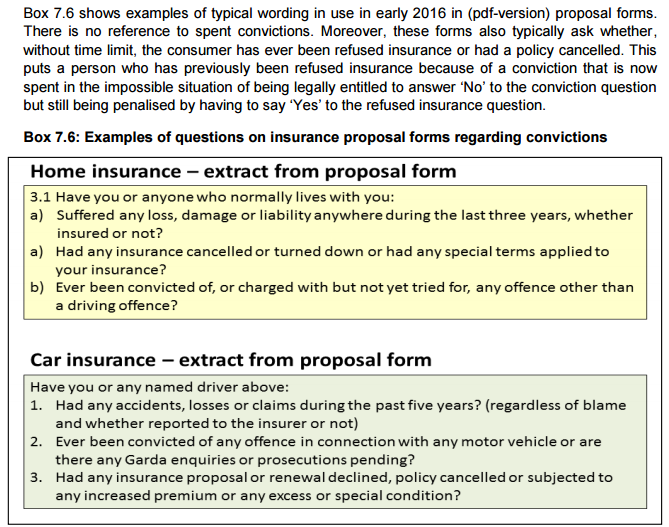

Extract from the FCA occasional paper

Although it didn’t name the companies involved, the FCA paper included two anonymous examples of current questions by home insurers and motor insurers.

Extract from the FCA occasional paper

The poor wording of questions by insurers is a major problem. Unlock’s helpline regularly gets contacted by people using insurance websites and asking us for clarity about what they do and don’t need to disclose. Very often, this is because the insurance company hasn’t made it clear that they don’t need to disclose convictions that are now spent under the Rehabilitation of Offenders Act 1974.

This is something we’re looking at. We’ve had one our helpline advisors do some research into the questions asked by insurers, and we’re in the process of pulling this together and analysing the findings.

As an aside, it was good to see a number of other issues featured in the occasional paper, including:

The numbers of people affected – In the infographic that the FCA used, they said that 750,000 people with unspent convictions and their families can struggle. This comes from a figure we presented a couple of years ago, and this is a conservative estimate of the numbers with unspent convictions. Although this figure is an underestimate for another reason – it doesn’t include those that are potentially covered by some of the misleading questions that insurers ask (see below). When this is taken into account, the numbers affected by the practice of insurers runs into the millions, given there’s over 10.5 million people in the UK with a criminal record.

Last month, the Centre for Entreprenuers (CfE) published some brilliant research, From inmates to entreprenuers, looking at the role of setting up businesses and how they can help to break the cycle of reoffending.

We were pleased to support the research by carrying out a survey alongside the CfE which had 158 responses from people with convictions in the community.

As part of the research, 83% said that having a criminal record made it harder to start a business, with 89% saying it made it harder to get insurance for your business.

I was asked to provide a comment for the report. I explained how we know that people with convictions face significant stigma and discrimination from employers as a direct result of their criminal record. Although more work needs to be done on combating this, entrepreneurship is an important alternative that, for some, is the right path towards a productive life as a law-abiding member of society. This research is an important contribution to this area and makes recommendations at both a strategic and operational level to maximise the opportunity that entrepreneurship provides people in achieving their potential.

Written by Christopher Stacey, Co-director of Unlock

Help us to scrap ‘disqualification by association’: The government are consulting on changes to the childcare disqualification arrangements

Ever since ‘disqualification by association’ (DbA) hit the headlines about 18 months ago, we have been working to try and scrap the regulations that have had a significant and unnecessary impact on the partners of those with a criminal record.

Earlier this month, the Department for Education (DfE) published a consultation with proposals for change. The deadline for responses to the consultation is 1st July 2016.

Find out more about the consultation, details of what we’re doing and how you can help on our information site.

Lord Ramsbotham introduces Private Members Bill to shorten rehabilitation periods

Lord Ramsbotham, Unlock’s President, has introduced a Private Members Bill into the House of Lords which would shorten the rehabilitation periods that apply under the Rehabilitation of Offenders Act 1974 (ROA).

The Bill, which had it’s first reading yesterday, proposes a number of changes. One of most significant elements is that sentences of over 4 years in prison would become spent 4 years after the end of the full sentence.

Although the Bill is a long way from becoming law, it’s a welcome step forward in getting further reform to the ROA back on the agenda.

Were the effects of accepting a caution explained to you? Send us a copy of what you were given

Our helpline receives enquiries every day from individuals who have accepted cautions without feeling like they understand the effects of it.

The Home Office guidance on cautions states that ‘the significance of the admission of guilt in agreeing to accept a caution must be fully and clearly explained to the individual before they are cautioned.’

However, different police forces give different guidance and have different forms in place.

We’re interested in seeing copies of cautions that people have accepted in the last two years. This will give us a good idea of the type of written information people were given before they signed to accept the caution.

We use cookies where necessary to allow us to understand how people interact with our website and content, so that we can continue to improve our service.

We only ever receive anonymous information, and cannot track you across other websites. Find out more

{kind=link}

{kind=link}

{kind=link}