Unlock, the leading charity for people with convictions, has today published new research which highlights major problems in the way that insurance companies deal with the criminal records of people applying for home insurance.

The charity looked at the approaches of 42 high-street insurance companies and found that two-thirds failed to make it clear to people that they didn’t need to disclose convictions that were ‘spent’ under the Rehabilitation of Offenders Act 1974. They also found that nearly 1 in 5 companies took into account a spent conviction when considering an application even though they were under a legal obligation to disregard it.

The research also highlights the blanket approaches taken towards applicants that declare a conviction. None of the companies gave any individual consideration online – 100% of the insurers refused to offer a policy online to an applicant that disclosed conviction, without any specific consideration about the relevance of the offence to the policy being taken out. Only one company offered a policy over the telephone.

Commenting on the research, Christopher Stacey, co-director of Unlock, said:

“We regularly get contacted by people who are confused by what they’re being asked to disclose when applying for insurance, and these findings show that when they mistakenly reveal something they didn’t need to, they’re getting punished for it. It doesn’t have to be this way, and insurance companies themselves are contributing to this problem.

“The insurance industry needs to update its good practice and insurers should implement clear and consistent wording in relation to asking about unspent convictions. Given that two-thirds of the insurers we looked at are not doing this at the moment, there’s a lot of work to do. That’s why we’ll be referring these findings to the Information Commissioners Office, as we believe insurers are breaching the principles of the Data Protection Act.

“For an industry that prides itself on assessing risk, it was astounding to find that all of the insurers blanketly refused to offer cover online where an unspent conviction was disclosed – there is clearly a widespread policy of ‘computer says no’. Given there’s nearly three-quarters of a million people in England & Wales with an unspent conviction, with thousands of people having convictions from decades ago that are still unspent, one has to ask whether insurers are taking a proportionate approach to risk by simply refusing to offer cover to people in this situation.”

Notes

- Press/media enquiries

- The research is available to download from Unlock’s website.

Coverage

The findings of this research were featured in:

Background

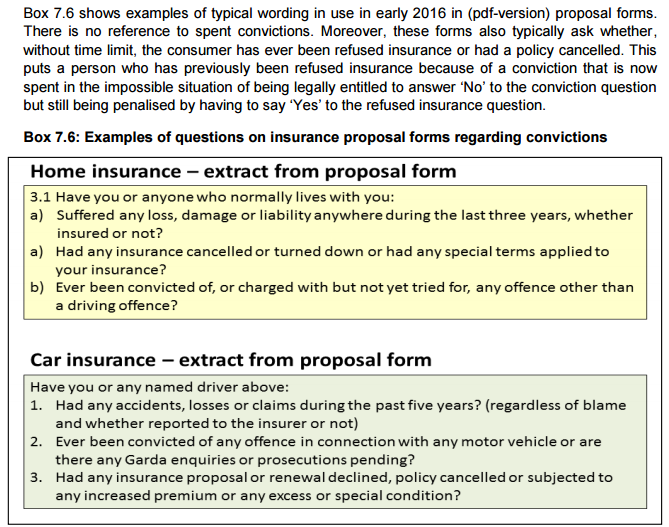

Insurance companies ask about criminal records when a person applies for cover across a range of insurance products, including buildings, contents, motor and public liability insurance. Convictions that are now ‘spent’ (as set out by the Rehabilitation of Offenders Act 1974) do not need to be disclosed for insurance purposes and they should not be taken into account by insurance companies when providing quotes.

Unlock’s helpline regularly receives enquiries from people with convictions that are looking for insurance. Common problems include:

- Individuals being unable to obtain quotes from mainstream insurance providers when they reveal that they’ve got a criminal record.

- Others with spent convictions being confused by the questions they are being asked by insurers, with many wrongly believing that spent convictions need to be disclosed and may be taken into account.

- Instances where insurers take into account spent convictions when they have a legal obligation to disregard them.

- Policies being withdrawn because, instead of asking a question, the insurer includes some form of “no convictions” statement in the assumptions of the quote. When the individual discovers this and informs the insurer, they revoke the policy.

Case study – Paula

Paula was convicted of an overpayment of benefits 6 years ago. She was given a 4 month suspended prison sentence. The conviction became spent around three and half years ago, because under the Rehabilitation of Offenders Act 1974, that sentence becomes spent 2 years after the end of the 4-month sentence.

“Pretty much straight after my conviction, we had to renew our home contents insurance, and our existing insurer refused to renew it because I told them of the conviction. The only companies we ended up being able to get quotes from were specialist brokers that specifically helped people with unspent convictions.

“When I was originally convicted, nobody told me when my conviction would become spent, or what that would mean at that point. So for the last 3 years, I’ve been continuing to use specialist brokers for my insurance.

“Recently, I tried to get a quote online through the Post Office, but I ticked the box about convictions because they asked “Has anyone in the property ever been convicted…?” – I thought the right answer was “yes”, because I had, and they were unable to give me a quote.

“It wasn’t until I spoke to Unlock that they told me that my conviction was now spent and that I didn’t need to tell insurance companies anymore. Two weeks ago, I went and got a quote from Admiral. They made it clear that they only needed to know about unspent convictions, so I could confidently answer “no” to that without feeling like I was doing anything wrong.

“Why don’t insurers make that clear when they ask you the conviction question on the quote form? For the last couple of years, I feel like I’ve been paying over the odds with specialist brokers when I could have been using mainstream comparison websites and getting a much better deal.” Paula

Case study – John

John was convicted of attempted murder in 1971. He got a life sentence. He’s been out of prison for nearly 30 years. But when he discloses that conviction to insurance firms, they refuse to cover the contents of his flat.

“In 1971, I was attacked and I retaliated a couple of weeks later. I was convicted of attempted murder. I got a life sentence. I was 23 years old.

“In 1986 I had a stroke and was discharged from prison and came to live here. I’ve lived here a number of years, and I can’t get household contents insurance. I’ve tried many times but because I answer the question “do you have any criminal convictions”, because I put “yes”, I’m declined insurance because they say that thee sentence isn’t spent. Well, it can’t be spent because I’m on life parole. So, the only way I can get insurance is to lie, but if I do lie and they find out, I’ll have paid money for years, possibly for nothing, becuase they will find any excuse not to pay out, and that would be a valid reason because I hadn’t answered the question truthfully.

“I just feel like I’m still being sentenced. I’m vulnerable because I’m now getting on; I’m 72 years of age. I would feel comfortable if I could have household contents insurance; I just want to insure the few bits and pieces I’ve got.

“I’ve been to a broker. The housing authority offer household insurance but they declined to insure me. I’ve been to Aviva, I’ve been to Direct Line. None of them will insure me because I have an unspent conviction. There are several politicians that have been to jail for fraud yet their convictions will be spent. Well mines never spent because it was a life sentence.

“How can I integrate with society if I can’t have household contents insurance. I feel like I’m missing. I think I should be treated as everyone else. I have been almost 30 years out of prison. I can get car insurance. I get travel insurance. Why can I not have household contents insurance? And why should I pay a higher premium? I think I should be treated just as Joe Bloggs in the street is treated, who’s 72 years of age, living in a local authority property and just gets on with life.” John

Responses from insurers

In response to Radio 4’s Money Box featuring the launch of the research, a number of insurers provided a comment to the BBC (see below)

Co-op

“We insure customers with spent convictions, and we apologise that in this instance we incorrectly declined the quote, which is not our standard policy.

“We are now implementing additional training to ensure that this doesn’t happen again.

“For customers that take out insurance online, we have a Q&A on our website to provide information on convictions. However we are also reviewing the wording within our quote process, to ensure that it is clear.”

esure/Sheila’sWheels

“esure and Sheilas’ Wheels do not ask customers to disclose spent convictions when they apply for a motor or home insurance policy. Our approach is entirely in line with the Rehabilitation of Offenders Act 1974.

“Spent convictions are therefore not taken into account in our underwriting or pricing policies regardless of the time when the conviction was spent.”

Aviva

“We want to help customers understand whether a conviction should be declared so we invite customers with previous convictions to phone in and speak to one of our experts to ensure there are no issues around non-disclosure.

“Aviva does not ask customers to declare spent convictions nor do we take into account spent convictions when offering home insurance.

“We continually review our customer journeys and later this year will be making some changes to our online home quote journey to ask customers only to consider unspent convictions, and we will be providing a link to Unlock so that customers are fully informed and are able to establish for themselves whether their conviction is spent or not.”

Littlewoods/Very

“Shop Direct introduces Very and Littlewoods Home Insurance to consumers, with the products sold by Ryan Direct Group and underwritten by Royal & Sun Alliance. We were unaware of this issue and would like to thank Money Box for bringing it to our attention. We have since reached out to Royal & Sun Alliance to understand more and will take any steps necessary to ensure that its practices are both fair and clear.”

LV

“We’d like to thank Unlock for bringing this issue to our attention, it is absolutely not our intention to decline customers with spent criminal convictions.

“The majority of our business comes from price comparison websites who all ask about unspent criminal convictions. Our website is in line with this, we ask about criminal convictions within the last 5 years and have text on the page explaining that we don’t need to know about spent criminal convictions.

“However, on the telephone, we simply ask for criminal convictions in the last 5 years. We recognise that this is not right and have already begun a process to educate staff on this matter. This will ensure they are aligned and there’s no risk of inadvertently considering spent criminal convictions.”

{kind=link}

{kind=link}

{kind=link}